PARSIPPANY, N.J (July 24, 2024) – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended June 30, 2024. Highlights include:

- Global RevPAR grew 2% in constant currency.

- System-wide rooms grew 4% year-over-year.

- Opened over 18,000 rooms globally, including over 7,000 in the S., which represented a year- over-year increase of 16%, and the first ECHO Suites Extended Stay by Wyndham.

- Awarded 180 development contracts globally, including 96 contracts in the S., which represented an increase of 33% year-over-year.

- Development pipeline grew 1% sequentially and 7% year-over-year to a record 245,000 rooms.

- Ancillary revenues increased 6% compared to second quarter 2023.

- Diluted earnings per share increased 30%, to $1.07, and adjusted diluted EPS grew 22%, to $1.13, or 12% on a comparable basis.

- Net income was $86 million for the second quarter, a 23% increase over the prior-year quarter; adjusted net income was $91 million, a 14% increase over the prior-year quarter.

- Adjusted EBITDA increased 13% compared with the prior-year quarter, to $178 million, or 6% on a comparable basis.

- Returned $162 million to shareholders through $131 million of share repurchases and quarterly cash dividends of $0.38 per share.

- Successfully completed the repricing of its Term Loan B Facility, reducing its interest rate by 60 basis points to SOFR plus 1.75%, and upsizing the facility by $400 million.

“The resilience and highly cash generative nature of our business model was once again on full display this quarter,” said Geoff Ballotti, president and chief executive officer. “Amid a normalizing domestic RevPAR environment, we delivered strong adjusted EBITDA driven by net room and ancillary fee growth. We awarded 33% more hotel contracts domestically which grew our development pipeline to a record 245,000 rooms, and drove significant increases in our U.S, international and global royalty rates. Year-to-date, we’ve returned over $250 million to shareholders, representing 4% of our beginning market capitalization this year.”

System Size and Development

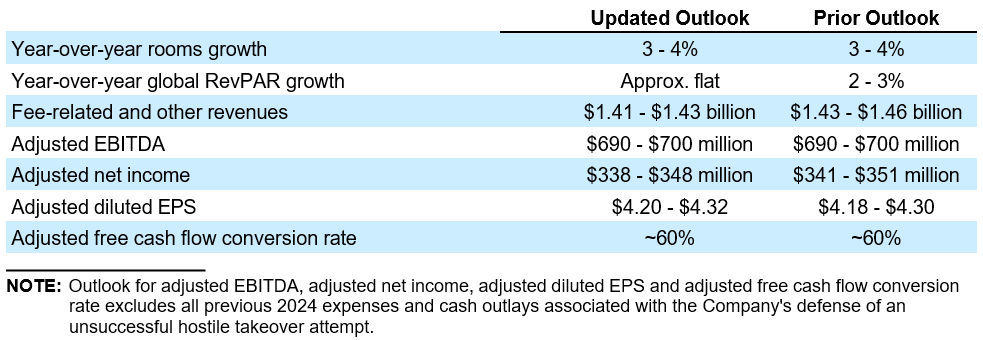

The Company’s global system grew 4%, reflecting 1% growth in the U.S. and 8% internationally. As expected, these increases included 3% growth in the higher RevPAR midscale and above segments in the U.S., as well as strong growth in the Company’s two highest international RevPAR regions, EMEA and Latin America, which grew 12% and 11%, respectively. The Company continued to improve its retention rate and remains solidly on track to achieve its net room growth outlook of 3 to 4% for the full year 2024.

On June 30, 2024, the Company’s global development pipeline consisted of approximately 2,000 hotels and 245,000 rooms, representing another record-high level and a 7% year-over-year increase. Key highlights include:

- 5% growth in the S. and 9% internationally

- 16th consecutive quarter of sequential pipeline growth

- Approximately 70% of the pipeline is in the midscale and above segments, which grew 4% year-over- year

- Approximately 14% of the pipeline represents ECHO Suites Extended Stay by

- Approximately 58% of the pipeline is international

- Approximately 79% of the pipeline is new construction, of which approximately 35% has broken ground

- During the second quarter of 2024, the Company awarded 180 new contracts, including 96 contracts in the U.S., which represented an increase of 33% year-over-year.

RevPAR

Second quarter global RevPAR increased 2% in constant currency compared to 2023, reflecting flat growth in the U.S. and 7% growth internationally.

In the U.S., the Company’s midscale and above segments grew RevPAR 2% year-over-year while RevPAR for its economy segment declined 2%. Overall, U.S. RevPAR results were driven by growth of 90 basis points in occupancy, partially offset by a decline of 50 basis points in ADR. Importantly, RevPAR growth in the U.S. accelerated during the second quarter, improving 520 basis points sequentially, including an improvement of 560 basis points for its U.S. economy brands.

Compared to 2019, which neutralizes the impact of COVID recovery timing, the Company grew RevPAR for its economy and midscale brands by 9% and 8%, respectively, while RevPAR for its upscale and above brands continued to lag 2019 by 2%.

Internationally, RevPAR for the Company’s Latin America, EMEA and Canada regions collectively increased 15% due to both continued pricing power, with ADR up 13%, and occupancy growth of 2%. RevPAR for the Company’s APAC region declined 12% primarily due to a difficult year-over-year comparison resulting from that region’s COVID recovery timing in second quarter 2023. APAC occupancy declined 7% and ADR declined 5%.

Compared to 2019, which neutralizes the impact of COVID recovery timing, the Company more than doubled the RevPAR for its Latin America, EMEA and Canada regions, while RevPAR for its APAC region continued to lag 2019 by 11%.

Second Quarter Operating Results

- Fee-related and other revenues were $366 million compared to $358 million in second quarter 2023, reflecting global net room growth of 4% and a 6% increase in ancillary revenue streams, partially offset by a $3 million decline in management fees, in part due to the exit of the Company’s S. management business.

- The Company generated net income of $86 million compared to $70 million in second quarter The increase was primarily reflective of higher adjusted EBITDA, a benefit in connection with the reversal of a spin-off related matter and a lower effective tax rate, partially offset by higher interest expense and restructuring costs.

- Adjusted EBITDA grew 13% to $178 million compared to $158 million in second quarter 2023. This increase included a $10 million favorable impact from marketing fund variability, excluding which adjusted EBITDA grew 6% primarily reflecting higher fee-related and other revenues, disciplined cost management given the recent RevPAR environment as well as a benefit from insurance recoveries.

- Diluted earnings per share was $1.07 compared to $0.82 in second quarter 2023. This increase reflects higher net income and the benefit of a lower share count due to share repurchase activity.

- Adjusted diluted EPS grew 22% to $1.13 compared to $0.93 in second quarter 2023. This increase included $0.09 per share related to expected marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased 12% year-over-year reflecting comparable adjusted EBITDA growth and the benefit of share repurchase activity partially offset by higher interest expense.

- During second quarter 2024, the Company’s marketing fund expenses exceeded revenues by $5 million, in line with expectations; while in second quarter 2023, the Company’s marketing fund expenses exceeded revenues by $15 million, resulting in $10 million of marketing fund The Company continues to expect marketing fund revenues to equal expenses during full-year 2024.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity

The Company generated $1 million of net cash provided by operating activities (inclusive of $42 million of payments related to the Company’s successful defense of a hostile takeover attempt) and generated adjusted free cash flow of $69 million in second quarter 2024. The Company ended the quarter with a cash balance of

$70 million and approximately $820 million in total liquidity.

The Company’s net debt leverage ratio was 3.5 times at June 30, 2024, the midpoint of the Company’s 3 to 4 times stated target range.

In May 2024, the Company successfully repriced and upsized its outstanding Senior Secured Term Loan B Facility (“Prior Term Loan B”). The new Senior Secured Term Loan B Facility (“New Term Loan B”) has an outstanding principal balance of $1.5 billion, which includes an upsize of $400 million. The facility has an interest rate of SOFR plus 1.75%, representing a 60 basis point reduction to the Prior Term Loan B.

Share Repurchases and Dividends

During the second quarter, the Company repurchased approximately 1.8 million shares of its common stock for $131 million. Year-to-date through June 30, the Company repurchased approximately 2.6 million shares of its common stock for $188 million.

The Company paid common stock dividends of $31 million, or $0.38 per share, during the second quarter 2024 and $63 million, or $0.76 per share, year-to-date.

The reduction in RevPAR and fee-related and other revenues reflects a more moderated RevPAR acceleration than previously anticipated. The reduction in adjusted net income represents an increase in interest expense due to the upsizing of the Company’s term loan B. This impact was more than offset in adjusted diluted EPS by second quarter share repurchase activity.

Year-over-year growth rates for adjusted EBITDA, adjusted net income and adjusted diluted EPS are not comparable due to full-year 2023 marketing fund revenues exceeding expenses by $9 million, which substantially completed the recovery of the $49 million support the Company provided to its owners during COVID. The Company continues to expect marketing fund revenues to equal expenses during full-year 2024 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.